Obtaining new customers is great for business unless they fail to pay you. This can be stressful, frustrating and put a great deal of pressure on business owners. That’s where credit control comes in.

If payment from the customer is not obtained and the goods or services have already been provided, your cash flow is likely to be under pressure. Ensuring that customers pay on time will make managing your business easier.

If you fail to pay your suppliers because you have not been paid by your customer, then you could also be damaging their business as well. This is not only bad business practice but could be regarded as corporate social irresponsibility. Treat your suppliers as you want your customers to treat you.

Factors to consider

The first thing you should do is get to know your customer. This should start before you take on a new customer and before you give them any credit.

The bare minimum of what you should know is:

Before you provide goods or services to any customer make sure you address the following:

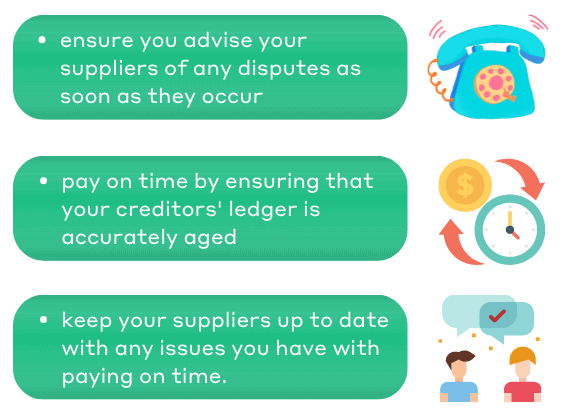

- discuss and agree payment terms with the customer before accepting the order

- agree the terms in writing

- review any documentation from the customer where they try to change the agreed payment terms

- negotiate and agree payment terms with suppliers before accepting the order

- if there is a gap between customer and supplier payment terms,consider whether finance is available to bridge the gap (this will require an understanding of your working capital management)

- produce a cash flow forecast covering all expected income and expenses

- have a standard credit control policy in place to ensure that payment terms cannot be altered without appropriate authorisation

- ensure that you have the right to apply late payment and interest charges on invoices.

After you have provided goods or services to a customer ensure that you:

- raise invoices promptly

- raise invoices accurately to ensure all items are included at the quoted prices

- include a reference number for the order and then quote this if any dispute arises

- have everything the customer requires on the invoice

- have a credit control process in place for chasing invoices

- have a process for dealing with disputes

- keep a log of disputes to ascertain whether similar disputes for customers occur

- ensure that your invoices are fully compliant with HMRC for VAT purposes.

Consider your suppliers – treat them as you would like to be treated

Remember that not paying your suppliers on time is a bad business habit and it may result in a drop in your credit rating. You should:

Some businesses unfortunately go ‘bad’ so you may wish to consider obtaining credit insurance where the business:

- would not be able to function if key customers went insolvent

- does not have the controls in place to ascertain whether acustomer is likely to go insolvent

- is struggling to obtain information on prospective customers

- needs to improve credit control management

- is considering a new market venture.

Businesses should consider obtaining factoring and financing options when:

- insufficient cash reserves are available to pay suppliers on time

- the business needs to grow

- the level of short term finance (including any overdraft facility) is insufficient

- staff do not have the right level of credit control management skills.

How Blue Spire can help

If you are struggling with your cash flow in these difficult times then we would be happy to discuss this further with you.

Please contact us for more detailed advice.