Following the Covid-19 pandemic, the working world has changed in many ways, from how we work to where we work. Most businesses now offer a more flexible approach with regards to working from home, or what is known as hybrid working – with employees splitting time between home and being on-site.

But what about the self-employed? What tax implications does homeworking have for them?

UK tax rules differ considerably depending on whether you are self-employed, as a sole trader or partner, or whether you are an employee, even if that is as an employee of your own company.

In this blog we take a look at tax relief and the implications of homeworking specifically for the self-employed.

Using your home as an office

If a self-employed individual carries out some of their business from home, then tax relief may be available to them. HMRC accepts that even if part of the business is done elsewhere, a deduction for part of the household expenses is still acceptable provided that there are times when part of the home is used solely for business purposes.

To quote HMRC:

Self-employed individuals pay tax on the profits that the business makes or their share of those profits. So, the critical issue is to ensure that costs incurred can be set against that profit. For day to day overheads, those costs generally have to be incurred ‘wholly and exclusively‘ for the purposes of the trade to be tax deductible.

So that there is no confusion, wholly and exclusively does not mean that business expenditure has to be separately billed or that part of the home must be permanently used for business purposes.

However, it does mean that when part of the home is being used for the business, then that is the sole use for that part at that time. HMRC accepts that costs can be apportioned but on what basis?

Well, if a small amount is being claimed then HMRC will usually not be too interested. In fact, HMRC seems to accept that an estimate of a few pounds a week is acceptable. However, if more is to be claimed, then HMRC suggests that the following factors are considered:

- the proportion in terms of area of the home that is used for business purposes

- how much is consumed where there is a metered or measurable supply such as electricity, gas or water and

- how long it is used for business purposes

What sort of costs can I claim for?

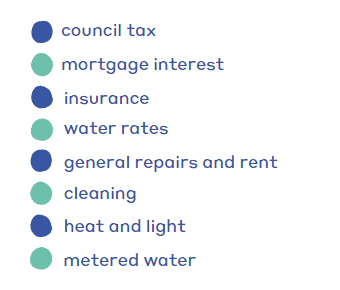

Generally, HMRC will accept a reasonable proportion of costs such as:

Other allowable costs may include the cost of business calls on the home telephone and a proportion of the line rental, in addition to expenditure on internet connections to the extent that the connection is used for business purposes.

So how does this work in practice?

As already mentioned, if there is a small amount of work done at home, a nominal weekly figure is usually fine but for substantial claims a more scientific method may be needed (see below example).

Visit here for more information on how to calculate your allowable expenses.

Equipment costs

For self-employed businesses, the depreciation of assets is covered by a set of tax reliefs known as capital allowances. For equipment at home, such as a laptop, desk, chair, etc, capital allowances may be available on the business proportion (based on estimated business usage) of those assets.

So, for example – if Andrew uses his laptop solely for business, the whole cost will be within the capital allowances rules.

What about travel costs?

Another consequence of working from home when you are self-employed, is the potential impact on travel costs. The cost of travelling from home to the place of business or operations is generally disallowed, as it represents the personal choice of where to live. The fact that the individual may sometimes work at home is irrelevant.

Where an individual conducts office work for their trade does not by itself determine their place of business, so although many may be able to claim tax relief for the costs of working from home, far fewer will be able to claim travel costs of going to and from their home office.

Of course, this principle presupposes that there is a business or operational ‘base’ elsewhere from which the trade is run. Normally, the cost of travel between the business base and other places where work is carried on will be an allowable expense, while the cost of travel between the taxpayer’s home and the business base will not be allowable.

However, where there are no separate business premises away from the home, travel costs to visit clients should be fully allowable. The crux of the matter is where the business is really run from.

Principal Private Residence Relief (PPR)

Capital gains tax contains a tax exemption for the sale of an individual’s private home, known as principal private residence relief (PPR). Where part of the dwelling is used exclusively for business purposes, PPR relief will not apply to the business proportion of the gain. However, HMRC makes clear in their guidance that ‘occasional and very minor’ business use is ignored.

Summary

There are many different options and things to take into consideration for claiming tax relief when self-employed, but the key is to be clear about the rules, keep good records and be sensible about how much to claim.

How Blue Spire can help

If you are self-employed and would like any help about obtaining tax relief on the costs of homeworking or other expenses, please contact us.