Earlier this month, the UK government announced a new plan for health and social care, which includes a temporary increase to National Insurance contributions, before the introduction of a separate Health and Social Care Levy.

The changes are estimated to raise £36bn over the next three years and will be used to help with social care and bring extra funding and additional support to the NHS.

What are the new plans?

From 6 April 2022 to 5 April 2023, National Insurance contributions will increase by 1.25%, and this increase will be spent on the NHS and social care in the UK.

The increase will apply to:

- Employees (Class 1 – Primary)

- Employers (Class 1, 1A and 1B – Secondary)

- Self-employed (Class 4)

If you are an employee

As an employee, you pay Class 1 (Primary) National Insurance contributions.

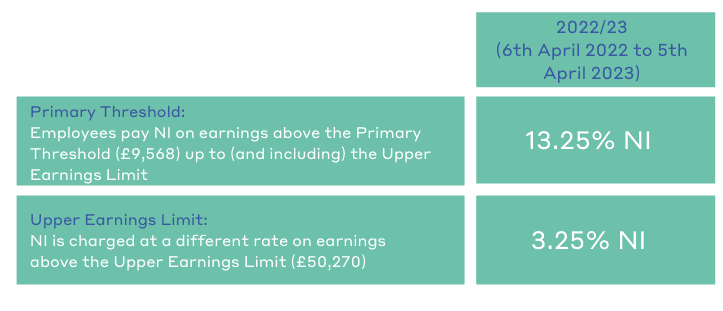

In the 2021-22 tax year, the National Insurance rates for most people are 12% for employees who earn over the Primary Threshold (£9568) and under the Upper Earnings Limit (£50,270), then an additional 2% above the Upper Earnings Limit.

The below table shows what the National Insurance and healthcare levy rates will be when the changes come into effect from 6 April 2022:

People earning under £9,564 a year, or £797 a month, don’t have to pay National Insurance and won’t have to pay the new levy.

How to pay

Your employer will deduct your National Insurance contributions with your tax from your wages before you get paid. Your monthly payslip will show your contributions.

How much more will employees pay

Our table below shows the National Insurance increase that employees will pay between 6 April 2022 – 5 April 2023:

If you are an employer

An employer will deduct an employees’ National Insurance contributions, and pay them to HMRC alongside their employer contributions.

The below table shows the rate of National Insurance that employer’s pay in the current tax year and what they will pay when the changes come into effect from 6 April 2022:

If you are self-employed

Self-employed individuals pay Class 2 and Class 4 National Insurance, depending on their profits.

The below table shows the rate of National Insurance that self-employed individuals pay in the current tax year and what they will pay when the changes come into effect from 6 April 2022:

If you are self-employed, you won’t pay the levy on any self-employed income below the £9,568 Lower Profits Limit threshold.

Self-employed individuals will pay the levy through their self-assessment tax return, as will anyone paying the levy along with dividend tax.

You might be an employee but also do self-employed work. In this case, your employer will deduct your Class 1 National Insurance from your wages, and you may have to pay Class 2 and 4 National Insurance contributions for your self-employed work.

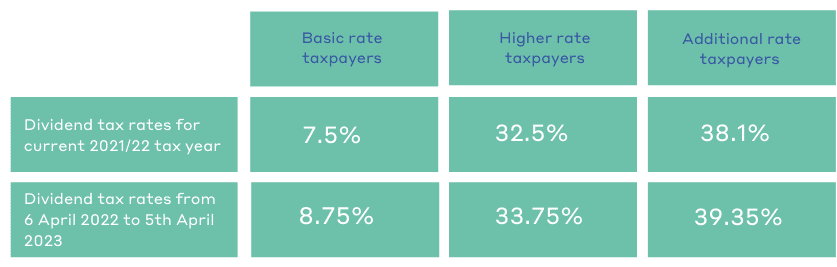

What changes will there be to dividend tax rates

The UK Government will also increase the rates of dividend tax from April 2022, which are payable on dividend earnings of above £2,000 per year.

What happens after April 2023

From April 2023, National Insurance will return to its current rate, and the extra tax of 1.25% will be collected as a seperate Health and Social Care Levy.

Individuals who are above State Pension age will not be affected by the temporary increase to National Insurance contributions for the 2022-23 tax year but will be liable to pay the levy from April 2023.

| If you have any questions or need advice on any of the above, then please do not hesitate to contact us. |