If you make supplies of goods or services to a customer but were not paid, you may be able to claim Bad Debt Relief from VAT on bad debts you have incurred.

Bad Debt Relief allows businesses who have made supplies that they have accounted for and paid VAT on, but have not received payment, to claim a refund of the VAT by reference to the outstanding amount.

The Conditions for Relief

In order to make a claim for Bad Debt Relief, a business must satisfy the following conditions:

- goods and services have been supplied and the VAT in question has been accounted for and paid

- 6 months has elapsed since the later of the date of supply and the due date for consideration, whichever is the later

- all or part of the outstanding amount must have been written off in the accounting records as a bad debt (in the ‘refunds for bad debts account’).

Making the Claim

A claim is made by entering the appropriate amount in Box 4 of the VAT return for the period in which entitlement to the claim arises (or any permissible later period).

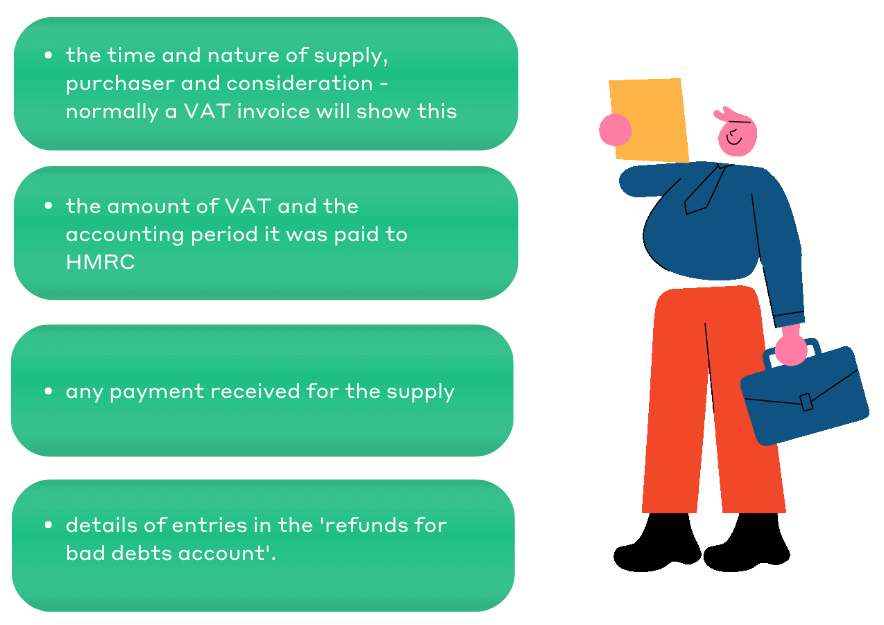

Records

Businesses making Bad Debt Relief claims must keep records for four years from the date of the claim to show:

Repayment of Input Tax by Purchaser

Where a customer has not paid a supplier within six months of the date of the supply or, if later, the date payment is due, VAT previously claimed as input tax, must be repaid.

This puts a burden on all VAT registered traders to monitor their transactions to anticipate whether they need to reverse any input tax recovered on goods received from suppliers.

How Blue Spire can help

We would be pleased to help with further advice in this area.

Please get in touch with us today or visit gov.uk for full guidance on Bad debt relief.