Making sure your taxes are correct as a Sole Trader, Trust or Partnership is always a challenge, but there are major changes coming, that could have an impact on the way many unincorporated businesses are taxed on their profits.

From the 2024/25 tax year, the basis period will be reformed, which will have wide-ranging implications for many UK businesses.

The government has decided to implement these changes as an attempt to simplify the reporting requirements for MTD for Income Tax.

The new rules can be complex, and may be difficult for some people to follow, so in this blog we will help to explain the changes around Basis Period Reform, and what they might mean for you and your business.

What is a Basis Period?

A Basis Period is the 12-month period for which businesses must calculate their taxes. Generally, businesses draw up annual accounts to the same date each year. This is called their ‘accounting date’.

Currently, a business’s profit or loss for a tax year is the profit or loss for the year up to their accounting date – for example, accounts drawn up to 30 April 2021 are taxed in the 2021/22 tax year.

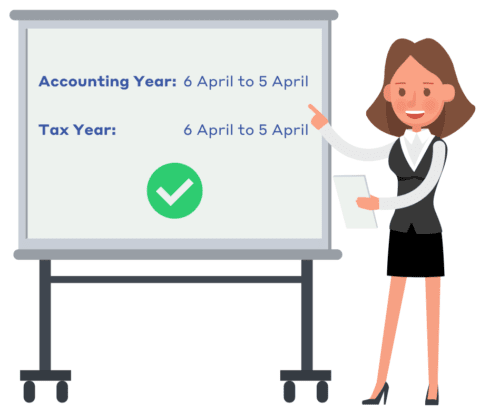

Depending on when a business begins trading, some individuals may choose to default to the tax year to decide their accounting date. This means their accounting period is therefore 6 April to 5 April the following year.

For those using the tax year as their accounting period, the basis period and the accounting period match.

The new rules that come into place from the 2024/25 tax year will affect businesses that have accounting dates and periods that don’t match the tax year (e.g. accounting periods that aren’t 6 April to 5 April).

Under the new Basis Period Reform system, businesses liable for income tax will be taxed on profits arising in a tax year, regardless of their accounting date.

Transitional year

These changes were originally due to come into effect a year earlier, but after a consultation period, the Government delayed the proposal to allow taxpayers to prepare for the transition to the new basis period.

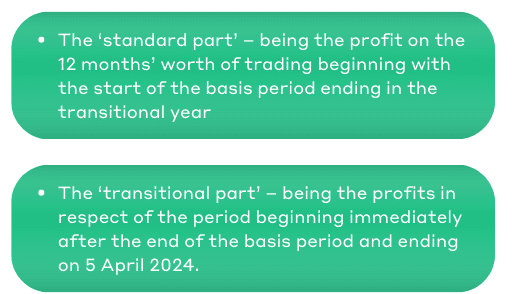

The 2023/24 tax year is going to be a transitional period for the Basis Period Reform. In the transitional year, businesses that do not have an accounting year end date between 31 March and 5 April will need to recognise two profit elements:

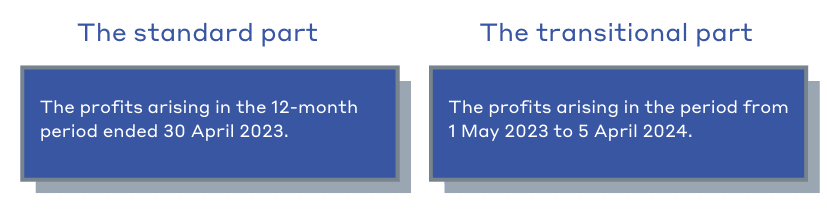

For example:

A business has a 12-month accounting period ending 30 April 2023. In the 2023/24 transitional year it will recognise:

Losses in the transitional year

If a loss arises in the transitional year, the taxpayer can treat the business as ceasing on 5 April 2024 for the purposes of the terminal loss relief rules. This means that this loss can be carried back for up to three tax years, rather than the standard 12 months, to offset against profits taxed in those years.

Overlap Relief

Overlap profits can occur in the first 2 or 3 years of trading, or in any year in which there is a change of basis period because of a change of the accounting date. This can create overlapping basis periods, which charge tax on profits twice. ‘Overlap relief’ can be claimed for this which is usually given when a business ceases to trade.

One of the aims of the new changes is to remove the need for the administration of overlap relief.

Under the new changes, if the business has any overlap profits, it must offset these against the profits of the 2023/24 tax year.

How the Basis Period Reform will impact businesses?

Businesses that currently use the tax year as their accounting year have nothing to worry about as no changes will be required.

But if your business has an accounting period that doesn’t match 6 April to 5 April the following year, then there are several potential issues:

- From the tax year 2024/25, you’ll have to calculate the taxes you owe based on the tax year, rather than your accounting period.

- Your accounting period for the year 2023/24 will be extended to fit in with the tax year, which could lead to a higher tax bill. Additionally, if you have any overlap profits from when you first started trading, you will need to find the documentation so this can be claimed back.

- It is possible to spread your 2023/24 transitional tax bill over five years but this will require some careful planning to ensure cash flow isn’t affected.

How can Blue Spire help?

The Basis Period Reform will take effect from the 2024/25 tax year, but with the transitional year approaching, it is vital that those affected start preparing sooner rather than later.

Blue Spire can help you to navigate these changes in good time.

| If you are concerned about how your business may be impacted by the Basis Period Reform, then please do not hesitate to get in touch with us today. |

Source: ICAEW