One of the most commonly asked questions we hear, is what accounting records a business must keep, and for how long.

This is not surprising, as record-keeping can represent a significant administrative burden with associated costs. It can also arise in penalties from HMRC should a business fail to keep the records that it is required to retain.

In this blog, we look at what records you need to keep, and for how long.

Limited companies

Limited companies are required to keep all records of any transactions that have been made that enable the financial position of the company to be determined with reasonable accuracy at any time.

The accounting records are required to contain entries from day to day of all sums of money received and expended by the company, and the matters to which they relate, as well as a record of the assets and liabilities of the company.

Additional requirements exist for those companies whose business involves dealing in goods, as they must retain a statement of the stock held at the end of the financial year, which includes supporting stocktaking records.

Unless a retail operation, there is also a requirement to maintain records of all goods sold and purchased, that includes and identifies the buyers and sellers.

A parent undertaking is obliged to ensure that any subsidiary undertaking also maintains adequate accounting records.

HMRC requirements

The Company law requirements for record keeping are primarily designed to enable directors to meet their obligation to prepare accounts each year for distribution to the company’s shareholders and filing with Companies House.

Additional requirements exist for all taxpayers, not just companies and LLPs, that enable them to demonstrate that their tax liabilities have been correctly calculated.

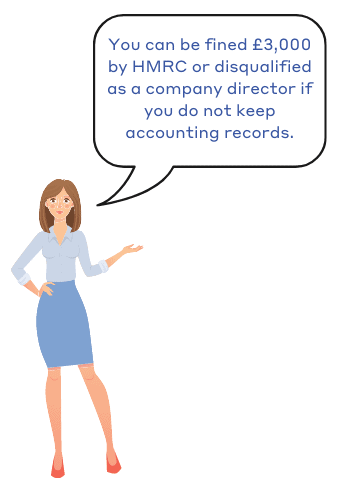

For businesses that fail to keep adequate records, HMRC have the power to issue civil penalties of up to £3,000.

In addition to meeting the Company law requirements, HMRC require companies to retain any other financial records, information and calculations that were used to prepare the annual accounts and its corporation tax return. This goes further than the Company law requirements and will include items such as:

- bank statements

- invoices

- contracts

It will also include details of judgements and estimates made when preparing the accounts that impact upon the calculation of the company’s tax liability, such as provisions for stock obsolescence and bad debts, accruals and prepayments, and the measurement of financial instruments. It can be particularly important to retain records such as these, as these are likely to form the basis of any HMRC enquiry into the company’s tax affairs.

How long to keep records

You must keep records for 6 years from the end of the last company financial year they relate to, or longer if:

- they show a transaction that covers more than one of the company’s accounting periods

- the company has bought something that it expects to last more than 6 years, like equipment or machinery

- you sent your Company Tax Return late

- HMRC has started a compliance check into your Company Tax Return

Individuals and partnerships

The requirements for individuals, whether they operate as individuals or in partnership with others, mirror those for companies.

The accounting records they are required to retain will be the same, although they are also required to retain records in support of other aspects of their self-assessment tax return such as dividend vouchers or interest statements.

For partnerships, the accounting records will be shared by all the partners of the business. A nominated partner should be appointed, and it will be their responsibility for managing the partnership’s tax returns and keeping business records.

The period that records need to be retained for differs slightly when compared to companies. Instead, they should be kept for at least 5 years after the 31 January submission deadline of the relevant tax year. If the tax return is submitted more than four years after the normal filing deadline, then records must be kept for 15 months after the tax return is filed.

Value Added Tax

All VAT-registered businesses are required to keep records of sales and purchases.

In addition, they must retain a ‘VAT account’, a separate record of the VAT charged on supplies made and paid on your purchases. The figures in the VAT account are used to complete the VAT return, and it must show the following:

• Total VAT sales

• Total VAT purchases

• The amount of VAT owed to HMRC, or which can be reclaimed

• If the VAT Flat Rate Scheme is being used, the flat rate percentage used and the turnover it applies to

• The VAT on any EU acquisitions (purchases) or dispatches (sales)

The VAT account will also need to record any adjustments made when calculating your VAT liability, for example in respect of partial exemptions calculation or the correction of errors discovered in earlier VAT Returns.

Generally, VAT records must be kept for 6 years, although supporting records for bad debt relief claimed is only required to be kept for four years.

Employers

All employers are required to keep payroll records in support of the amounts paid to staff. This will include the following:

• Amounts paid to employees and the deductions made. As well as PAYE and national insurance, this will include student loan repayments, pension contributions, payroll giving donations and child maintenance payments.

• Employee leave and sickness absences

• Tax code notices

• Taxable expenses or benefits

• Payroll giving scheme documents, including the agency contract and employee authorisation forms

• Reports and payments made to HMRC

It would also be sensible to retain other records in support of the operation of your payroll, such as employment status determinations, compliance with national minimum wage requirements and the checks you undertake to ensure that your employees have a right to work in the UK.

Payroll records must be kept for 3 years from the end of the tax year to which they relate.

Format of records

Accounting records can be kept in physical form, electronically or as part of a software program such as accounting software.

Whatever format is used, records must be easy to retrieve in a readable format. Where software is required to retrieve records it is important to remember to retain access to that software for the minimum period for keeping records – for example, ensuring that any necessary licence fees are paid.

Increasingly though, certain records must be retained in digital format, to support HMRC initiatives such as Making Tax Digital. To date, this only applies to VAT, and requires VAT registered businesses that have adopted Making Tax Digital to retain the records used to prepare the VAT return for filing in digital form.

However they are stored, accounting records should be kept in an orderly fashion that helps to ensure that records are complete and accurate, and capable of timely retrieval. Also, it is imperative that you follow the rules on data protection wherever personal information forms part of your accounting records.

How Blue Spire can help

We will be very pleased to discuss with you the impact these record-keeping requirements may have on your business.

If you would like to discuss these issues in more detail, please do not hesitate to contact us.